A BOLD Merchant Statement Breakdown: Part Two

Read Part I of the Series Here

Read Part I of the Series Here

This post is a continuation of a two-part blog series on Merchant Statements. We discuss what every processor should know about statements, how to uncover hidden fees, and a sneak peek into the BOLD. Statement Analysis process.

As mentioned in part one of this blog series, it is key for both the merchant and the processor to remember that every statement looks different. They can come in different formats or sizes while also using varied terminology or abbreviations. Bottom line, the best thing you can do as a processor is know what the rates are and what they should be. And as you’re looking through your statement, you can see what doesn’t match up. You discover the padding if things don’t match up.

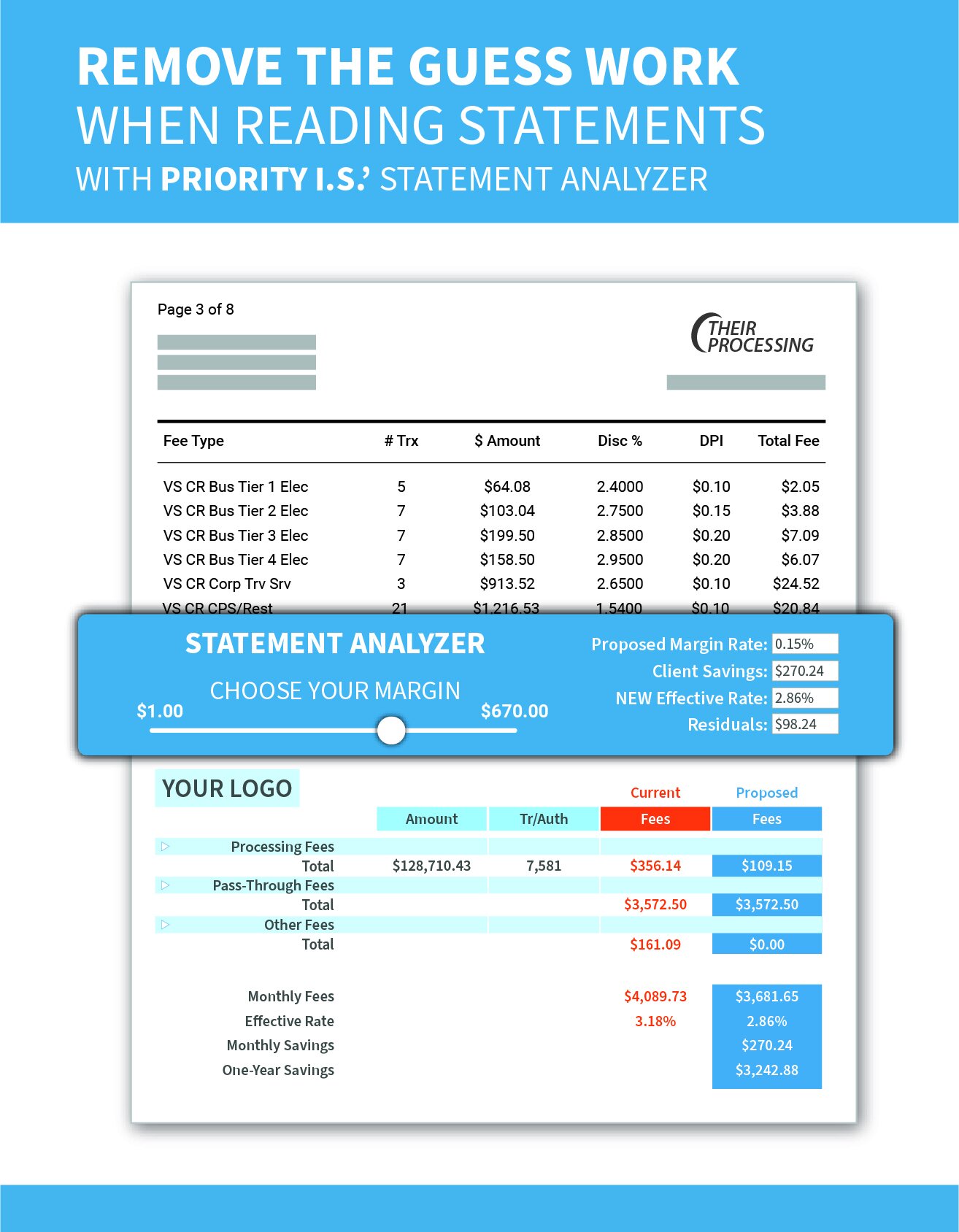

Uncovering Hidden Fees

Typical ways processors are able to pad hidden fees is primarily through interchange. Due to a lack of transparency, deceptive statements make it difficult to identify hidden fees, and therefore, make it easy to fall into its trap. This brings us to a very important question: Are there any tricks to uncovering hidden fees? Gary Liu, President of ISV/VAR Channel for BOLD., says, “At the end of the day, it’s not a trick… it’s math.” Below, you can find links to Visa and Mastercard’s Interchange breakdown.

VISA USA INTERCHANGE REIMBURSEMENT FEES

MASTERCARD 2021-2022 U.S. REGION INTERCHANGE PROGRAMS AND RATES

A Transparent Approach

At BOLD, we start our statement analysis with math. We take a look at four different sectors of fees: Processing fees, Authorization/Transaction fees, Monthly fees, and Interchange. We take the first three fees and subtract them from the total effective rate to determine whether or not hidden fees exist.

Next, we match what the merchant is currently being charged to give our partners insight as to what profit would look like if it remained the same. With that, we also offer the freedom to modify what the merchant’s statement looks like. Whether it’s a simple adjustment or completely cutting out something, we want to give a broader perspective on ways the partner could save the merchant money while maximizing their profitability.

After receiving a statement, our team will provide an analysis and proposal within 48 hours. To receive your Statement Analysis, submit a case below with your attached statement or email our PRM team at prm@boldpay.io.

Recent Comments